Table 1. Key Metrics.

| Company (Ticker) | Amazon.com, Inc. (AMZN) |

| Sector | Consumer Discretionary[1] |

| Industry | Broadline Retail[2] |

| Market Capitalization | Mega Cap ($2.37T)[3] |

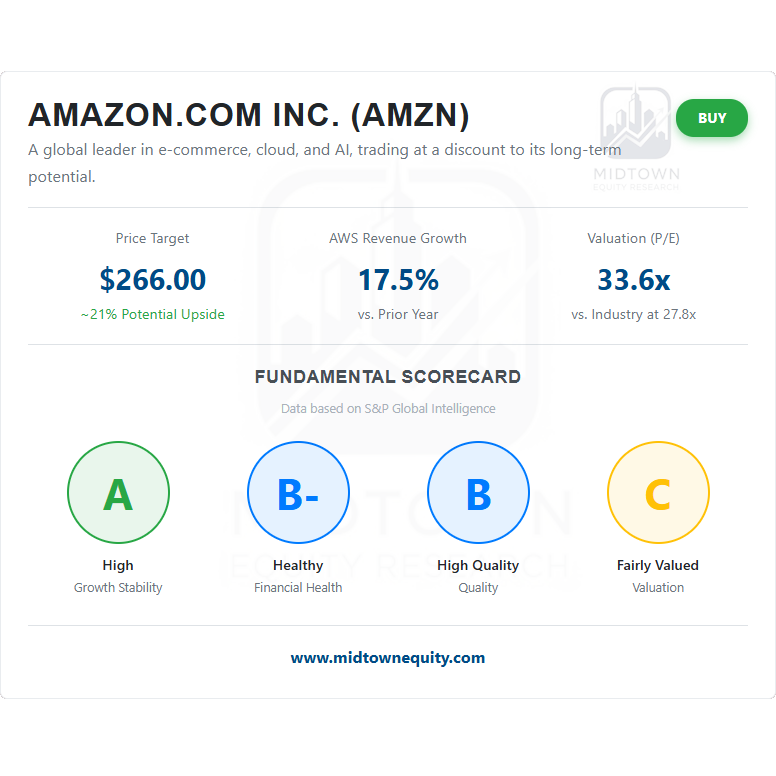

| Current Price | $219.76[6] |

| Analyst Price Target | $266.00[7] |

| Potential Upside | ~21% |

| YTD Performance vs. Market | –0.7% vs. +15.5%[4] |

| YTD Performance vs. Sector | –0.7% vs. +6.8%[4] |

| Dividend Yield | 0.00%[1] |

| Valuation | Neither Undervalued nor Overvalued (49/100)[13] |

| Quality | Slightly High (61/100)[13] |

| Growth Stability | High (89/100)[13] |

| Financial Health | Neither Unhealthy nor Healthy (60/100)[13] |

1. Overview: More Than Just Cardboard Boxes | Unpacking the Undervalued Amazon Stock Thesis

When you think of Amazon (AMZN), what comes to mind? Is it the smiley-faced boxes that magically appear on your doorstep? While that’s a huge part of their story, it’s like judging an iceberg by what appears on the surfance. Here at Midtown Equity Research, we see this company as a sprawling tech empire hiding in plain sight, not simply a large retailer. Indeed, Amazon is a behemoth in the Consumer Discretionary sector,[1] and, with a market capitalization of around $2.37 trillion, it’s firmly in the “Mega Cap” category, rubbing shoulders with the largest companies in the world.[2], [3] Let’s be honest that its year-to-date performance has been a bit of a snooze, down -0.7% while the S&P 500 has climbed over 15%.[4] And that, my friends, is exactly what gets our contrarian senses tingling about this potentially undervalued Amazon stock.

On the surface, its earnings metrics look solid, with a trailing twelve-month (TTM) earnings per share (EPS) of $6.55.[5] For instance, its TTM price-to-earnings (P/E) ratio sits around 33.6x, which is a tad higher than the Broadline Retail industry average of n, suggesting a premium valuation.[6] Because it is a growth-obsessed company, Amazon reinvests every penny, so it doesn’t pay a dividend and has a dividend yield of 0.00%.[1] And with a market beta of around 1.3 to 1.4, the stock is theoretically 30-40% more volatile than the broader market, which is pretty standard for a company in a cyclical sector.[1], [7] But these numbers only tell part of the story. To see the real value, we have to pop the hood and look at the engine. That’s where our tagline, “Look Deeper. Invest Wiser,” really comes into play.

2. Recent News: Market Jitters vs. Long-Term Plays

Amazon’s recent news cycle is a perfect case study in market short-sightedness. For instance, on July 31, 2025, the company reported stellar second-quarter earnings. It posted an EPS of $1.68, absolutely crushing analyst estimates of $1.33 by over 26%.[4] In addition, net sales soared 13% year-over-year to $167.7 billion, also comfortably beating expectations.[5] And every segment fired on all cylinders: North America sales grew 11%, International surged 16%, and the crown jewel, Amazon Web Services (AWS), posted a solid 17.5% growth.[5] So, the stock rallied, right? Nope. Not even close.

Guidance, Spending, and a Major Outage

In after-hours trading, the stock tumbled. The reason? Management’s guidance for third-quarter operating income came in between $15.5 billion and $20.5 billion, a little weaker than Wall Street’s crystal ball had hoped.[5], [9] This guidance spooked investors, but it points directly to the core of our bull thesis. The perceived weakness isn’t due to a failing business; rather, it’s the direct result of Amazon’s massive, strategic spending spree on Artificial Intelligence. The company has signaled it plans to spend over $100 billion on capital expenditures, primarily to build out the data centers and infrastructure needed to dominate the next generation of computing.[5]

Adding to the recent drama, a major AWS outage on October 20 knocked thousands of popular applications and websites offline for over 15 hours.[10], [11] The disruption originated from a DNS resolution issue in the US-EAST-1 data center, affecting core services like DynamoDB and causing a cascading failure across the internet.[10], [12], [13] Despite the global impact, the market’s reaction was surprisingly muted; Amazon’s stock actually rose 2.6% in the following session, suggesting investors viewed the event as a temporary operational hiccup rather than a fundamental flaw.[14], [15]

Insider Moves and Ecosystem Expansion

Meanwhile, the company continues to expand its ecosystem like a digital octopus. With recent announcements that include expanded collaborations with major players like Accenture, the NBA, and Nasdaq, alongside the rollout of new AI tools like Bedrock AgentCore and services like in-office Amazon Pharmacy kiosks.[5], [16] Of course, we have to address the elephant in the room: insider selling. Reports show a significant number of sales from top executives, including founder Jeff Bezos, over the past year, with zero open-market buys.[17], [18] While this can look alarming, context is key. Many of these sales are executed under pre-scheduled Rule 10b5-1 trading plans for diversification and to fund other ventures—a common practice for executives whose wealth is heavily concentrated in one stock.[19] For a mature, mega-cap company, periodic, planned selling by tenured executives is more akin to routine financial management than a red flag signaling imminent doom.

3. Fundamental Analysis: Why the Math is Misleading for Undervalued Amazon Stock

This is where we at Midtown Equity Research really roll up our sleeves and justify our thesis! A quick glance at some quantitative models might make you scratch your head. S&P Global Market Intelligence, for instance, gives Amazon a Valuation score of 49.[13] According to the standard scale, that’s squarely in the “neither undervalued nor overvalued” camp. Similarly, its Financial Health score of 60 is also neutral,[13] and other models, like ISS-EVA, flag it as “less attractively priced.”[14] So, how on earth can Midtown Equity argue for an undervalued Amazon stock? Simple: these models are trying to measure a three-dimensional company with a one-dimensional ruler.

The Valuation Puzzle: A Sum Greater Than Its Parts

Valuing Amazon as a single entity is a fundamental mistake. In reality, it’s at least three distinct, powerhouse businesses rolled into one ticker symbol, and the market is failing to appreciate the sum of its parts.

- Amazon Web Services (AWS): This isn’t a retail division; it’s a high-growth, high-margin cloud computing goliath that should be valued like a top-tier software company.

- Amazon Advertising: A rapidly growing, incredibly profitable digital ad business that sits at the holy grail of commerce—the point of sale. It deserves a valuation multiple similar to Google or Meta.

- Retail Operations: The massive, lower-margin e-commerce and physical store business that everyone knows and uses.

Figure 1. Amazon vs it’s competitors.

When you value AWS and Advertising with the premium multiples they deserve and add the more modest value of the retail arm, the implied total value—a “sum-of-the-parts” valuation—comes out significantly higher than Amazon’s current market cap. While its trailing P/E of ~33.6x seems high, its forward P/E is projected to fall to ~29x by 2026 as earnings grow, making the price much more reasonable relative to its future potential.[8], [21] This hidden value is the core of our thesis and a classic example of why you need to Look Deeper.

Quality, Growth, and Health: The Trifecta of Excellence

Beyond the valuation argument, Amazon’s underlying fundamentals are simply best-in-class. For example, S&P Global rates its Quality at 61 (Slightly High) and its Growth Stability at a stellar 89 (High).[6] Similarly, Jefferson Research concurs, rating its Earnings and Cash Flow Quality as “Strong” and its Balance Sheet Quality as “Strongest.”[22]

The numbers absolutely back this up. For example, Amazon boasts a strong Return on Equity (ROE) of about 24% and an EBITDA margin of 20.3%, which absolutely dwarfs the sector median of just 4.9%.[2], [6] Its high growth stability score comes from remarkably consistent EPS and operating cash flow trends, providing a predictability that reduces risk for long-term investors.[6] Financially, the company is a fortress. Its debt-to-equity ratio is low and falling, and its interest coverage ratio is a staggering 60.85—meaning it earns nearly 61 dollars for every dollar it owes in interest payments, compared to a sector median of just 3.62.[6] These fundamentals suggest that the company is illustrating superhero-level financial strength.

Head-to-Head with the Competition: Not Even a Fair Fight

To truly appreciate Amazon’s dominance, just look at how it stacks up against other companies in the retail space. Honestly, it’s not even a fair fight (see Figure 1. Amazon vs it’s competitors above and Table 2. Amazon metrics versus it’s competitors below).

Table 2. Amazon metrics versus it’s competitors.

| Metric | Amazon (AMZN) | Target (TGT) | Best Buy (BBY) | Macy’s (M) | Groupon (GRPN) |

|---|---|---|---|---|---|

| Market Cap | $2.37T[3] | $42.3B[23] | $16.7B[2] | $4.8B[2] | $819M[2] |

| P/E Ratio (TTM) | 33.6x[8] | 11.0x[2] | 22.8x[2] | ~10.4x[24] | -14.17[25] |

| Revenue Growth (Y/Y) | +10.9%[2] | -0.95%[23] | – | -3.44%[24] | -4.3%[25] |

| Net Profit Margin | 10.5%[2] | 3.71%[23] | 4.6%[2] | 2.18%[24] | -12.0%[25] |

| Return on Equity (ROE) | 24.8%[2] | ~9.8%[23] | – | ~13.6%[24] | – |

This table makes it crystal clear: Amazon operates on a different planet in terms of scale, growth, and profitability. Therefore, comparing it to traditional retailers is like comparing a spaceship to a bicycle. Both are forms of transportation, but that’s where the similarities end.

4. Technical Analysis: Reading the Tea Leaves for Undervalued Amazon Stock

While our thesis is fundamentally driven, it’s always wise to check the technical picture to understand the market’s current mood. Think of it as checking the weather before a long road trip. According to analysis from Trading Central, the short-term sentiment for Amazon stock is currently bearish.[26] This view is based on a few key indicators that suggest some downward pressure in the immediate future.

The analysis identifies a key pivot point at $220.24. As long as the price stays below this level, the technical preference is for a move lower, with support levels at $214.65 and a primary target of $213.22.[26] This bearish outlook is supported by the Relative Strength Index (RSI), which is below its neutral 50 mark, and the Moving Average Convergence Divergence (MACD), which is negative and below its signal line. In simpler terms, the momentum indicators are pointing down for now. However, should the price manage to break above the $220.24 pivot, the next resistance levels to watch are $222.64 and $224.08.[26]

Here’s our take on the sentiment across different time horizons:

- Short-Term (2-6 weeks): Weak. The technical indicators point to potential for a limited decline or consolidation. This is the market noise we’re talking about.

- Mid-Term (6 weeks – 9 months): Neutral. The stock has been trading in a range, and the conflicting signals (like being below its 20-day moving average but above its 50-day) suggest a period of indecision.

- Long-Term (9+ months): Strong. We view any short-term technical weakness not as a warning sign, but as a fantastic opportunity to initiate or add to a position in this undervalued Amazon stock at a more attractive price, aligning with our strong fundamental conviction.

Figure 2. Short-term technicals vs. long-term fundamentals.

5. Analyst Ratings: A Resounding Chorus of ‘Buy’ for Undervalued Amazon Stock

If our fundamental analysis represents our deep dive, then the consensus from Wall Street analysts is the resounding chorus. And that chorus is singing a very, very bullish tune. Across the board, the sentiment from independent research firms is overwhelmingly positive, forming a strong pillar of support for the argument that Amazon stock is poised for a significant move higher.

According to data from Business Insider, out of 100 analysts covering the stock, a staggering 96 rate it a “Buy,” with only 4 assigning a “Hold” and a grand total of zero recommending a “Sell.”[27] This level of conviction is rare for any company, let alone one of Amazon’s size. This is echoed by other top-tier research providers; Refinitiv reports a strong “Buy” consensus from 71 analysts, and Zacks Investment Research gives AMZN its highest short-term rating of “1-Strong Buy” and a long-term “Outperform” recommendation.[5], [2]

This bullish sentiment is backed by ambitious price targets. The median 12-month price target from analysts sits around $266, with some estimates reaching as high as $300.[2], [28] Based on the current price, that median target implies a potential upside of over 20%. This isn’t just mild optimism; it’s a strong vote of confidence from the professional analyst community that the stock is currently undervalued relative to where they see it heading over the next year. It seems we’re not the only ones who think this undervalued Amazon stock is a bargain.

Figure 3. analyst ratings on amazon stock.

6. Risks & Counterarguments: Playing Devil’s Advocate on the Undervalued Amazon Stock Thesis

No analysis is complete without stress-testing the thesis. At Midtown Equity Research, we believe that understanding the bear case is crucial for making a wise investment decision. After all, ignoring risks is a recipe for disaster, and frankly, it’s just lazy analysis. So, let’s tackle the legitimate concerns about Amazon stock head-on, because true conviction comes from staring the counterarguments in the face and not flinching.

The Cloud Wars and Concentration Risk

First, the primary risk revolves around the two things that make Amazon great: AWS and its boundless ambition. The cloud wars are heating up. While AWS is still the market leader, its recent growth of ~18% has lagged behind Microsoft Azure’s 39% and Google Cloud’s 32%.[5] This has led to legitimate fears of market share erosion in Amazon’s most profitable segment, a concern frequently highlighted by Wall Street analysts.[29] The major AWS outage on October 20 serves as a stark reminder of the operational risks. That incident highlighted the internet’s heavy reliance on a few key providers and, more specifically, on AWS’s US-EAST-1 region, which has been implicated in multiple major outages over the last five years.[30], [31], [32]

The Staggering Cost of Ambition

Second, the cost of that ambition is staggering. The planned $100+ billion in capital expenditures to win the AI race is causing significant near-term pain.[5] It’s a key reason for the weak operating income guidance, and it has led to a dramatic 66% year-over-year decline in free cash flow.[5] This cash flow compression is a serious point that bears rightly flag. Finally, there’s the risk of Prime saturation in key markets and the ever-present shadow of regulatory scrutiny, which could target any of its dominant business lines.[5], [33]

Our analysis, however, indicates the market is misinterpreting these risks with a short-term lens. The massive AI spending isn’t just an “expense” that hurts margins; it is a strategic *investment* building the essential infrastructure for the next decade of technological growth. Years ago, Amazon sacrificed profits to build an untouchable logistics network for its retail empire. Today, it is sacrificing near-term margins to build the dominant platform for artificial intelligence. This spending is both a defensive moat to protect its lead and an offensive weapon to capture future AI workloads.[34] The current stock price reflects the market’s punishment for this long-term strategy, and that, in our view, is the very definition of a value opportunity for this undervalued Amazon stock.

7. Additional Notes: The Hidden Profit Engine in Undervalued Amazon Stock

Beyond the main pillars of retail and AWS, there’s another powerful engine humming within Amazon that often gets overlooked but is becoming increasingly important to the investment thesis: the advertising business. This isn’t just a side hustle; it’s a high-margin juggernaut that could be a significant driver of future profitability and a key reason we’re so bullish on Amazon stock.

In the most recent quarter, Amazon’s advertising services grew by a robust 23% year-over-year to $15.6 billion.[5] Some analysts, like Daniel Kurnos of Benchmark, believe the ad business can “grow faster than AWS and achieve higher margins.”[35] What gives it this incredible potential? Its strategic position. Unlike ads on Google (which capture search intent) or Meta (which target social interests), Amazon’s ads are placed directly at the point of sale. They target customers who are logged in, have their payment information saved, and are actively looking to make a purchase. This proximity to the transaction results in incredibly high conversion rates, making it an indispensable tool for the millions of third-party sellers on its platform.

Consequently, this advertising revenue flows through the income statement at very high margins, providing a powerful boost to Amazon’s overall profitability. As this segment continues to scale, it will provide yet another powerful stream of cash flow to fund the company’s ambitious growth projects in AI, healthcare, and beyond. It’s a critical piece of the puzzle that reinforces the idea that the future earnings power of this undervalued Amazon stock is being underestimated by the market today.

8. Summary: Why We Believe Undervalued Amazon Stock is a Titan in Disguise

In conclusion, Amazon presents a compelling case as an undervalued titan hiding in plain sight. While the market is fixated on short-term margin compression from strategic AI investments and intensifying competition, it appears to be overlooking the bigger picture. The company’s dominant positions in e-commerce, cloud computing, and digital advertising remain firmly intact. Moreover, the massive capital expenditure, while painful in the short term, is laying the groundwork for another decade of leadership in the age of AI. With a fortress balance sheet, exceptional growth stability, and an overwhelming vote of confidence from Wall Street analysts, the recent stock price stagnation offers a rare opportunity to invest in a world-class company at a reasonable valuation. The short-term technical weakness and negative sentiment around guidance have created what we believe is an attractive entry point for patient, long-term investors who can, as our tagline says, Look Deeper. Invest Wiser.

Amazon’s stock seems to be at a crossroads. Is the heavy spending on AI a brilliant long-term move or a drag on near-term profits? Do you see this undervalued Amazon stock as a deep value play or a value trap? Let us know your thoughts in the comments below!

This post is for informational and educational purposes only. It is not financial advice. Please conduct your own research and consult with a licensed financial advisor before making any investment decisions. Midtown Equity and its staff do not own an individual position in AMZN at the time of this publication, but do own this position indirectly via passive and active indices.We’re not just analysts; we’re investors too, but that doesn’t mean you should follow us off a cliff—please do your own homework so you can Think Deeper. Invest Wiser!

9. References

- Argus Research Company. 2025. “AMAZON.COM INC (NAS:AMZN).” Argus A6 Report, October 22, 2025.

- Financial Times. 2025. “Amazon.com Inc.” Accessed October 23, 2025. markets.ft.com/data/equities/tearsheet/summary?s=AMZN:NSQ.

- Investopedia. 2024. “How Can I Use Market Capitalization to Evaluate a Stock?” Last updated May 2, 2024. www.investopedia.com/ask/answers/042415/how-can-i-use-market-capitalization-evaluate-stock.asp.

- Zacks Investment Research. 2025. “Amazon.com Inc. (AMZN).” Zacks Equity Research Report, October 23, 2025.

- The Wall Street Journal. 2025. “Amazon.com Inc.” Accessed October 23, 2025. www.wsj.com/market-data/quotes/AMZN.

- Fidelity Investments. 2025. “AMZN – Amazon | Dividends & Earnings.” Data as of October 23, 2025.

- LSEG. 2025. “AMAZON.COM INC (AMZN-O).” LSEG Stock Reports Plus, October 22, 2025.

- Fidelity Investments. 2025. “AMZN – Amazon | Dividends & Earnings.” Data as of October 23, 2025.

- Massar, Carol, and Tim Stenovec. 2025. “Amazon Sinks on Weak Profit Outlook.” Bloomberg Surveillance (podcast), July 31, 2025. www.youtube.com/watch?v=DqkAsHHNlb8.

- NASDAQ. 2025. “AMZN Insider Activity.” Accessed October 23, 2025. www.nasdaq.com/market-activity/stocks/amzn/insider-activity.

- Quiver Quantitative. 2025. “Amazon Stock (AMZN) Opinions on Q3 2025 Financial Results and Automation Plans.” Last updated October 23, 2025. www.quiverquant.com/news/Amazon+Stock+%28AMZN%29+Opinions+on+Q3+2025+Financial+Results+and+Automation+Plans.

- Stock Titan. 2025. “Amazon Com SEC Filings.” Accessed October 23, 2025. www.stocktitan.net/sec-filings/AMZN/.

- S&P Global Market Intelligence. 2025. “Fundamental analysis for AMZN.” Data provided via Fidelity Investments as of October 23, 2025.

- ISS-EVA. 2025. “AMAZON.COM INC AMZN.” PRVit Company Report, October 23, 2025.

- Jefferson Research. 2025. “AMAZON.COM INC. (NASDAQGS AMZN).” Financial Sonar Report, October 17, 2025.

- LSEG. 2025. “LSEG I/B/E/S Estimates: AMAZON.COM INC (AMZN).” Report prepared October 23, 2025.

- Google Finance. 2025. “Target Corp (TGT:NYSE).” Accessed October 23, 2025. www.google.com/finance/quote/TGT:NYSE.

- Investing.com. 2025. “Macy’s Inc Financial Ratios.” Accessed October 23, 2025. www.investing.com/equities/macys-ratios.

- NASDAQ. 2025. “Groupon, Inc. Common Stock (GRPN) Financials.” Accessed October 23, 2025. www.nasdaq.com/market-activity/stocks/grpn/financials.

references Continued:

- Trading Central. 2025. “Technical Event Outlook – Amazon.com intraday: eye 213.22.” Report prepared October 22, 2025.

- Business Insider. 2025. “Amazon Stock, AMZN.” Accessed October 23, 2025. markets.businessinsider.com/stocks/amzn-stock.

- Forbes. 2025. “Amazon (AMZN).” Accessed October 23, 2025. www.forbes.com/companies/amazon/.

- Ji, Christine. 2025. “Amazon’s stock comeback hinges on AWS hitting this magic number. Why analysts are cautious.” MarketWatch, October 15, 2025. www.morningstar.com/news/marketwatch/20251015210/amazons-stock-comeback-hinges-on-aws-hitting-this-magic-number-why-analysts-are-cautious.

- Morningstar. 2025. “Amazon (AMZN) Stock Quote.” Accessed October 23, 2025. www.morningstar.com/stocks/xnas/amzn/quote.

- Spatacco, Adam. 2025. “Prediction: 1 Artificial Intelligence (AI) Stock Will Be Worth More Than Amazon and Palantir…” Nasdaq, October 23, 2025. www.nasdaq.com/articles/prediction-1-artificial-intelligence-ai-stock-will-be-worth-more-amazon-and-palantir.

- Ji, Christine. 2025. “Why Amazon’s stock is a ‘must add’ ahead of earnings, according to this analyst.” MarketWatch, October 22, 2025. www.morningstar.com/news/marketwatch/20251022162/why-amazons-stock-is-a-must-add-ahead-of-earnings-according-to-this-analyst.

- aboutamazon.com. 2025. “Amazon’s Official Website.” Accessed October 23, 2025. www.aboutamazon.com/.

- Times of India. 2025. “Amazon Web Services outage: What brought the internet down across the world for more than 15 hours.” October 21, 2025.

- The Guardian. 2025. “The Guardian view on the cloud crash: an outage that showed who really runs the internet.” October 22, 2025.

- The Register. 2025. “AWS outage exposes Achilles heel: central control plane.” October 20, 2025.

- The Indian Express. 2025. “What caused the AWS outage.” October 21, 2025.

- Investopedia. 2025. “Dow Jones Today.” October 21, 2025.

- Bitget. 2025. “AWS Outage Shakes Crypto: Impact on Amazon Stock and the Future.” October 23, 2025.

- Ookla. 2025. “AWS Outage Q4 2025.” October 21, 2025.

- The Indian Express. 2025. “What the AWS outage reveals about the internet’s backbone.” October 21, 2025.

- The Indian Express. 2025. “Amazon.com cloud service returned to normal operations.” October 21, 2025.

- Associated Press. 2025. “What to know about the Amazon cloud outage that exposed the internet’s vulnerable backbone.” October 21, 2025.

Leave a Reply